Closing entries to pass before preparing a Profit and Loss Account

Closing entries in accounting refer to the many entries that are made after an accounting year to eliminate the balances of all temporary accounts established throughout the accounting period and transfer their balances to the appropriate permanent accounts.

The process involves resetting the balances of temporary accounts to zero, ensuring their readiness for usage in the next accounting period.

Simultaneously, the balances of balance sheet accounts are adjusted accordingly. The process sometimes referred to as “closing the books,” is recognized in the field, and its regularity may differ depending on the company’s scale.

Closing entries

We have already seen the entries required to prepare the Trading Account and transfer the gross profit to the Profit and Loss Account.

To complete the Profit and Loss A/c, the undermentioned entries will be necessary.

(a) For items to be debited to the Profit and Loss Account -here profit and loss account will be debited, and respective expenses and losses will be credited. For ex:

Profit and Loss A/c Dr.

To Salaries A/c

To Rent A/c

To Interest Account

To Other Expenses Account

(b) Items to be credited to profit and loss account – Here, items representing incomes and gains shall be credited to the profit and loss account by debiting the particular income and crediting the profit and loss account as follows:

Bad Debts Recovered Account Dr.

To Profit and Loss Account

(c) Transfer to Profit and Loss account to the capital account – after items to be debited and credited have been transferred to the profit and loss account. The next step is to find out the difference between the totals and transfer the net profit or net loss to the capital account as follows:

- If the credit side is greater than the debit side, i.e. net profit, the entry will be:

Profit and Loss Account Dr.

To Capital Account

In the debit side is greater than the credit side, i.e. net loss, the entry will be:

Capital Account Dr.

To Profit and Loss Account

Adjustments Before Preparing Profit and Loss Account

At the time of preparation of the profit and loss account, there may be that some expenses are outstanding while a few others are prepaid. In the profit and loss, account items only for the current year should be debited or credited as the case may be.

We need to pass a few adjusting entries to eliminate the effect of outstanding or prepaid expenses or income.

The following entries are to be passed for adjustment:

(1) Expenses accrued and outstanding, e.g., Salaries, Wages, Taxes, Rent, etc.

| Appropriate Expense Account | Dr. |

| To Expenses outstanding Account | Cr. |

(2) Income accrued and receivable, e.g., Interest on Bonds, Fees, Rents and Premiums on leases, etc.

Income Receivable Account Dr.

To Appropriate Income Account

(3) Carrying forward income received in advance, e.g., Subscription in the case of an NPO or fees in case of the professional person.

Particular Income Account Dr.

To Income Received in Advance Account

(4) Carrying forward payments made in advance, e.g., Telephone, Rent, Insurance, etc., amount of which stand debited to an expense account.

Expenses Prepaid Account Dr.

To Particular Expenses Account

(5) Adjustment of stock of materials at hand, e.g., Stationery, Material, Manufacturing Stores, etc., the cost of which already has been debited to an expense account.

The stock of Materials Dr.

To Particular Expenses Account

Note: Next year, on the first day entries No. (1) to (5) should be reversed

(6) Provision for Bad and Doubtful Debts:

Profit and Loss Account Dr.

To Provision for Bad and Doubtful Debts Account

Note: The accounts of the customers concerned shall not be effected until the amount is actually written off for which the entry is,

Bad Debts Account Dr.

To Customer’s A/c

This entry is to be passed only if the actual bad debt has been written off; otherwise, entry (6) should also be reversed.

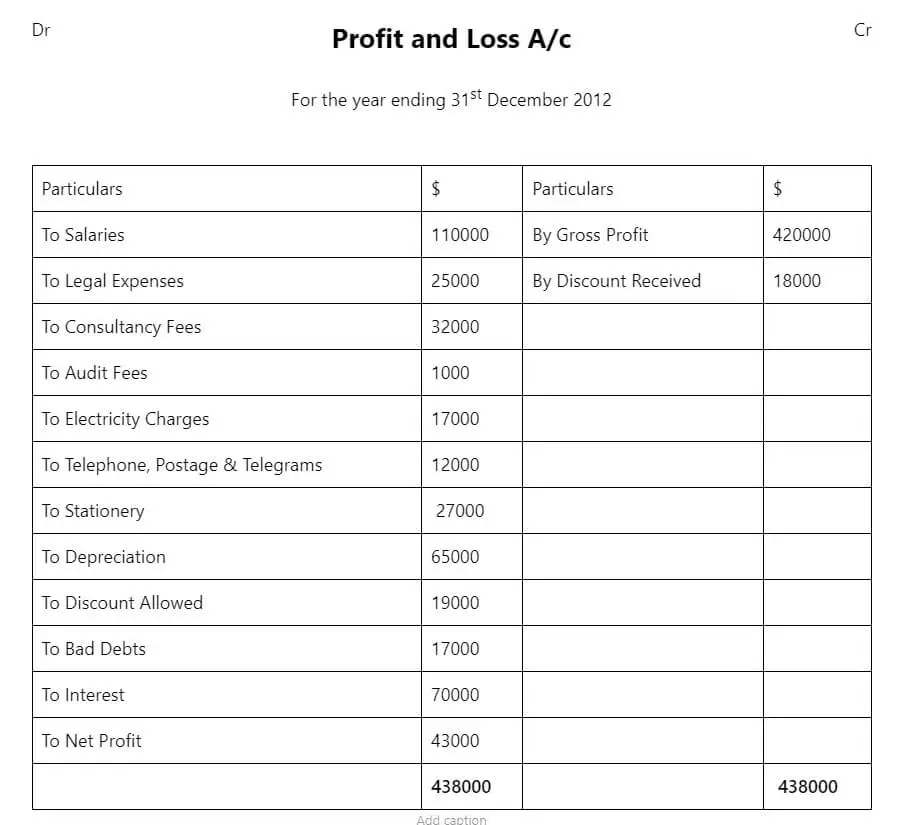

Illustration

On the basis of the data given below, prepare a profit and loss account for the year ending 31st December 2012

Gross Profit $420,000, Salaries $ 110,000, Discount (Cr.), $18,000, Discount (Dr.) $19,000, Bad Debts $ 17,000, Depreciation $65,000, Legal Charges $25,000, Consultancy Fees $32,000, Audit Fees $ 1,000, Electricity Charges $17,000, Telephone, Postage and Telegrams $12,000, Stationery $27,000, Interest paid on Loans $70,000.

Solution