Target Costing and Lifecycle Costing Explained

Target Costing and Lifecycle Costing are two important tools that can be used to manage and control costs throughout the product development process.

Target costing is a tool that can be used to set a target cost for a product or project. This target cost is then used as a cost management and control baseline. Lifecycle Costing is a tool that can be used to track and manage costs throughout the product development lifecycle.

Typically, conventional costing attempts to calculate the cost of creating an item by integrating the costs of currently used or consumed resources. Therefore, for each unit created, the conventional variable costs of material, direct labour and variable overheads are included (the total of these being the marginal cost of production), coupled with a part of the fixed production costs.

The fixed production costs can be included using a conventional overhead absorption rate (absorption costing (AC)), or they can be accounted for using activity-based costing (ABC). ABC is more complex but almost certainly more accurate. However, whether conventional overhead treatment or ABC is used, the overheads incorporated are usually based on the budgeted overheads for the current period.

Once the total absorption cost of units has been calculated, a markup (or gross profit percentage) is used to determine the selling price and the profit per unit. The markup is chosen so that the organisation should profit if the budgeted sales are achieved.

Flaws in Traditional Costing System

There are two flaws in this approach:

- The product’s price is based on its cost, but no one might want to buy it at that price. The product might incorporate features that customers do not value and therefore do not want to pay for. Competitors’ products might be cheaper or offer better value for money. This flaw is addressed by target costing.

- The costs incorporated are the current costs only. They are the marginal costs plus a share of the fixed costs for the current accounting period. Other important costs may not be part of these categories, but without which the goods could not have been made.

Examples include the research and development costs and any close-down costs incurred at the end of the product’s life. Why have these costs been excluded, particularly when selling prices have to be high enough to ensure that the product makes an overall profit for the company? To make a profit, total revenue must exceed total costs in the long term. This flaw is addressed by lifecycle costing.

Target Costing

Target costing is a process that involves setting cost levels needed to meet the target price. Target costing effectively reduces manufacturing costs by focusing on the most efficient ways of manufacturing while minimising the manufacturing lead time. The target cost approach occurs at every point during the production process, starting with planning where savings are identified. It also focuses on production by identifying the necessary changes to the design, layout, and procedures to reduce costs.

Target costing is very much a marketing approach to costing. The Chartered Institute of Marketing defines marketing as:

‘The management process responsible for identifying, anticipating and satisfying customer requirements profitably.’

In marketing, customers rule, and marketing departments attempt to find answers to the following questions:

- Are customers homogeneous, or can we identify different segments within the market?

- What features does each market segment want in the product?

- What price are customers willing to pay?

- To what competitor products or services do our customers compare ours?

- How will we advertise and distribute our products?

Marketing says that there is no point in management, engineers and accountants sitting in darkened rooms dreaming up products, putting them into production, adding on, say, 50% for markup, and then hoping those products sell. At best, this is corporate arrogance; at worst, it is corporate suicide.

Note that marketing is not passive, and management cannot simply rely on customers volunteering their ideas. Management should anticipate customer requirements by developing prototypes and other market research techniques. Of course, there will probably be a range of products and prices, but the company cannot dictate to the market, customers or competitors. There are powerful constraints on the product and its price, and the company has to make the required product, sell it at an acceptable and competitive price and, at the same time, make a profit.

If the profit is going to be adequate, the costs have to be sufficiently low. Therefore, instead of starting with the cost and working to the selling price by adding on the expected margin, target costing will start with the selling price of a particular product and work back to the cost by removing the profit element. This means that the company has to find ways to not exceed that cost.

Lifecycle Costing

When aiming to earn a profit on a product, the total income derived from the product must surpass overall costs, whether these costs are incurred before, during or after the product is produced.

This is the concept of lifecycle costing, and it is crucial to know that target costs can be driven down by tackling any of the costs that correspond to any portion of a product’s life.

There are four principal lessons to be learned from lifecycle costing:

- All costs should be considered when working out the cost of a unit and its profitability.

- Attention to all costs will help reduce the cost per unit and help an organisation achieve its target cost.

- Many costs will be linked. For example, more attention to design can reduce manufacturing and warranty costs. More attention to training can machine maintenance costs. More attention to waste disposal during manufacturing can reduce end-of-life costs.

- Costs are committed and incurred at very different times. A committed cost is a cost that will be incurred in the future because of decisions that have already been made. Costs are incurred only when a resource is used.

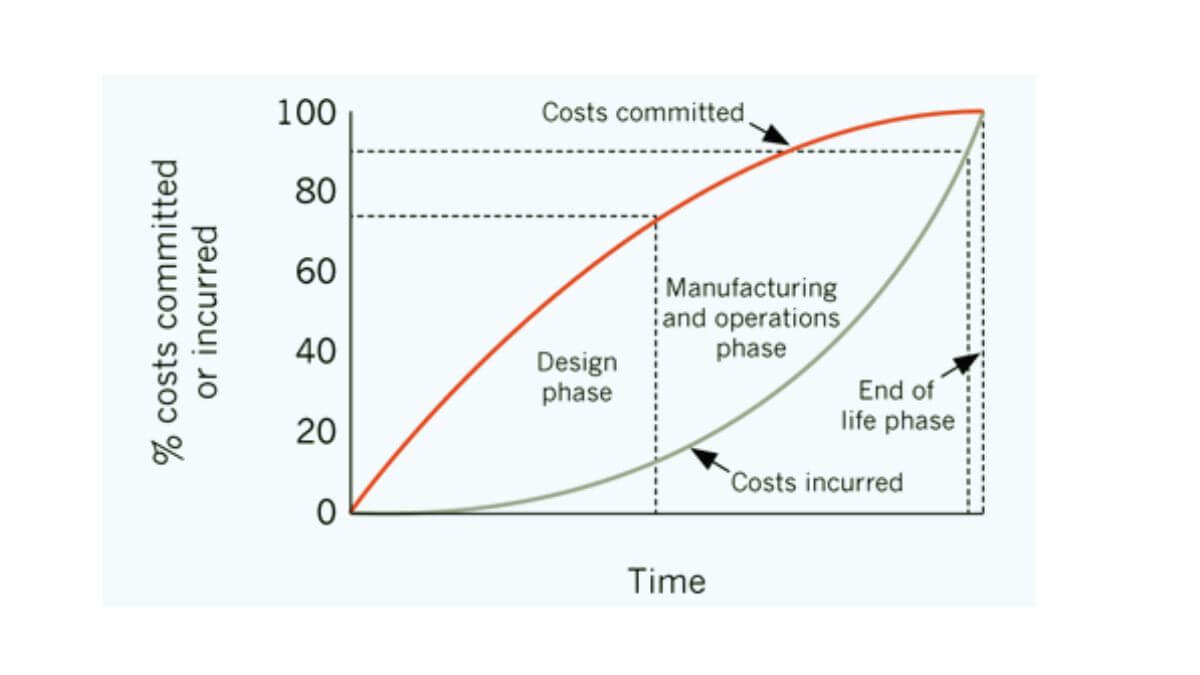

Typically, the following pattern of costs committed and costs incurred are observed:

The diagram shows that by the end of the design phase, approximately 80% of costs are committed. For example, the design will largely dictate material, labour and machine costs. The company can try to haggle with suppliers over the cost of components but if, for example, the design specifies 10 units of a certain component, negotiating with suppliers is likely to have only a small overall effect on costs.

A more considerable cost decrease would be obtained if the design had specified only eight units of the component. The design phase locks the company into most future costs, and this phase gives the company its most significant opportunities to reduce those costs.

Conventional costing records costs only as incurred, but recording those costs is different from controlling those costs and performance management depends on cost control, not cost measurement.