IFRS 1 First time Adoption of International Financial Reporting Standards sets out the processes that a company must take when it adopts IFRSs for the first time as the foundation for compiling its general purpose financial statements.

The IFRS offers certain exemptions from the general obligation to comply with each IFRS effective at the conclusion of its initial IFRS reporting period.

A revised version of IFRS 1 was released in November 2008 and applies if an entity’s first IFRS financial statements are for a period beginning on or after 1 July 2009.

Definition of first-time adoption

A first-time adopter is an organisation that declares explicitly and unequivocally for the first time that its general purpose financial statements comply with IFRSs.

A business may be a first-time adopter if it created IFRS financial statements for internal management use in the prior year and did not make such IFRS financial statements available to owners or external parties such as investors or creditors. If a business makes a set of IFRS financial statements available to owners or external parties in the prior year for whatever reason, the entity is already deemed to be using IFRSs, and IFRS 1 does not apply.

However

An entity is not a first-time adopter if, in the preceding year, its financial statements asserted:

- Compliance with IFRSs even if the auditor’s report contained a qualification with respect to conformity with IFRSs.

- Compliance with both previous GAAP and IFRSs.

An organisation that implemented IFRSs in a prior reporting period but did not include an explicit and unqualified statement of compliance with IFRSs in its most recent preceding annual financial statements may opt to:

- implement the requirements of IFRS 1 retroactively (including the different authorised exclusions), or

- implement IFRSs retrospectively in line with IAS 8 Accounting Policies, Changes in Accounting Estimates, and Errors, as if they had never ceased to apply IFRSs.

Adjustments required to move from previous GAAP to IFRSs at the time of first-time adoption

- Derecognition of some previous GAAP assets and liabilities

- Recognition of some assets and liabilities not recognised under previous GAAP

- Reclassification of some balance sheet items

- Measurement principles

Disclosures in the financial statements of a first-time adopter

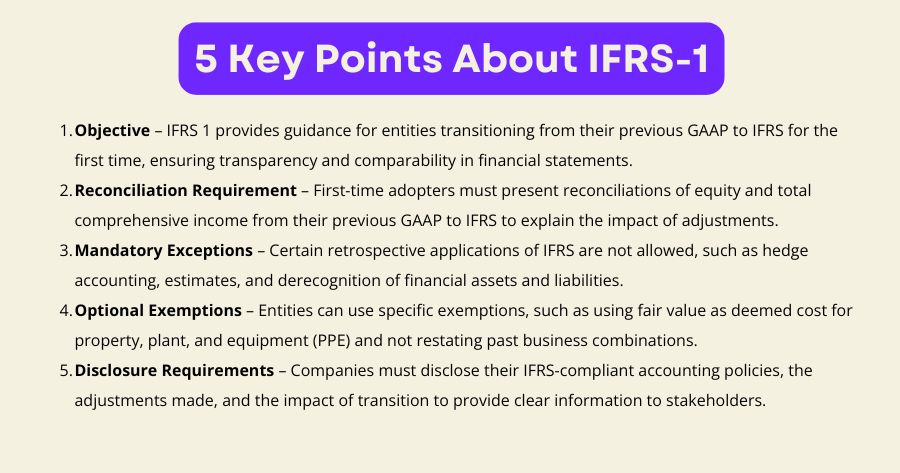

If a company is issuing its financial statements for the first time in accordance with International Financial Reporting Standards (IFRS), it will be required to meet the requirements of IFRS 1: First-time Adoption of International Financial Reporting Standards.

This standard states how entities should make the changeover from their existing Generally Accepted Accounting Principles (GAAP) to IFRS so that it will be transparent and comparable.

1. Reconciliation of Financial Statements

The company must present reconciliations to help users understand the transition from previous GAAP to IFRS. These reconciliations should include:

a) Reconciliation of Equity

- As at the date of transition (beginning of the earliest comparative period)

- As at the end of the last period presented under previous GAAP

b) Reconciliation of Total Comprehensive Income

- For the most recent annual period reported under previous GAAP

These reconciliations should highlight adjustments made due to IFRS adoption.

2. Explanation of Adjustments

The entity must provide detailed explanations of how IFRS adoption affected its financial position and performance, including:

- Adjustments due to new measurement criteria (e.g., fair value accounting)

- Changes in classification of financial instruments or assets

- Recognition of previously unrecorded liabilities or assets

3. Accounting Policies

The company must disclose the IFRS-compliant accounting policies applied in the first IFRS financial statements and explain any changes from previous GAAP.

4. Use of Exemptions and Exceptions

IFRS 1 allows certain exemptions and mandatory exceptions when transitioning to IFRS. The entity must disclose:

- The optional exemptions it has used (e.g., fair value as deemed cost, cumulative translation differences exemption)

- The mandatory exceptions applied (e.g., retrospective application of IFRS prohibited for derecognition of financial instruments)

5. Estimates Disclosure

If there were changes in estimates due to IFRS adoption, the company must disclose the nature of these changes and the reasons behind them.

6. Interim Financial Reports

If an entity presents interim financial reports in its year of adoption, it must reconcile the equity and total comprehensive income for interim periods, similar to annual disclosures.

Conclusion

First-time adoption of IFRS calls for extensive disclosures to provide transparency, comparability, and clarity to investors and stakeholders. Disclosures enable users to comprehend the effect of IFRS on financial performance and position, fostering confidence in financial reporting.