A ledger, in bookkeeping and accounting, is a fundamental record, containing all the financial transactions of a business, organized by account.

It essentially forms the spine of the accounting system by ingesting data from several financial documents and expressing them as a single coherent record. The ledger gives an orderly and detailed look at the financial activities of a company, which is so important to track income, expenses, and overall health.

Let’s explore what is the ledger and the purposes it serves in the bookkeeping and accounting functions and what are rules of posting to/from ledger.

Benefits of Ledger

A ledger is very useful and provides valuable information to the organisation. The net result of all transactions regarding a particular account on a given date can be ascertained only from the ledger.

For example, the proprietor on a particular date wants to know the amount due from a specific customer or the amount the firm has to pay to a specific supplier and such information can be found only in the ledger. Such information is very complex to ascertain from the journal because the transactions are recorded in chronological order and are not classified.

For easy posting and location, accounts are opened in the ledger in some specific order. For example, they can be opened in the same order as they appear in the profit and loss account or the balance sheet.

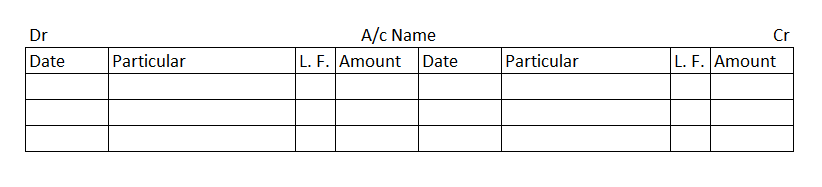

Format of A Ledger Account

A ledger account has two sides-debit (left part of the account) and credit (right part of the account). Each of the debit and credit sides has four columns. (i) Date (ii) Particulars (iii) Journal folio, i.e. page from where the entries are taken for posting and (iv) Amount.

As per this format, the columns will contain the information given below:

The title of the Account: It indicates the name of the particular account.

Dr. /Cr.: it refers to the debit or credit aspect of the transaction.

Date: The date of transactions is posted in chronological order in this column.

Particulars: The name of the accounts and events concerning the original book of entry is written on the debit/credit side of the account.

Journal Folio: It records the page number of the Journal on which the relevant transaction is recorded. This column is filled up at posting and not a recording.

Amount: This column is used to fill the amount of the transaction as recorded in the Journal.

Rules of Posting to Ledger

Posting the Debit Side of the Entry

When an account is debited in the journal, that amount should be written in the debit side of the account in the ledger too. In the particulars column, the name of the opposite account that was credited should be prefixed with the word “To.”

For example, in case of the journal entry “Cash A/c Dr. ₹10,000 To Sales A/c ₹10,000”, Cash Account will show “To Sales A/c ₹10,000” on the debit side.

Posting the Credit Side of the Entry

If any account is credited in the journal, then it should also be posted on the credit side of that account in the ledger. In the particulars column, the account which was debited is recorded preceded with the term “By”. For this example, Sales Account will display “By Cash A/c ₹10,000” on its credit side. This maintains that each component of the transaction is recorded correctly on both sides.

One Entry Per Account Per Transaction

Each account should only post a journal entry one time. Even if an account shows up in multiple entries, in one journal entry, each ledger account will be posted only one time. This prevents duplication and keeps the integrity of the financial information organized.

Use of Accurate Dates

The date appearing in the journal must also be recorded in the ledger for the corresponding transaction. This is useful when tracing an event relevant to a verification, auditing, or even preparing financial statements. Maintaining consistency in the entry of dates reinforces dependability and openness with regards to the accounting documents.

Balancing an Account

At the end of each month and year-end, all accounts in the ledger are balanced. Balancing here means ascertaining the net balance of all debit and credit transactions in a particular account.

For the accounts having nature in debit balance, we use ‘by balance c/d’ read as ‘by balance carried down’. On the opening date of the new month, the same balance is written as ‘To balance b/d’ read as ‘To balance b/d’. Similarly, for accounts having a balance in credit nature, balancing is done by writing ‘To balance c/d’ and at the beginning of the new month ‘By balance b/d’ is written.

However, nominal accounts are not balanced at the end of the year; they are transferred to Profit & Loss A/c (Trading A/c in case of Direct expenses). Hence, they have no opening balance at the beginning of the year. Only personal and real accounts can show balances.

Conclusion

In summary, a ledger is the core of your accounting system. It’s where all your financial transactions are recorded, organized, and analyzed, giving you a clear picture of your financial health and making informed decisions for your business or personal finances.